In the first article of this Sustainability Reporting series, we clarified the legal context set by the European Union regarding transparency on sustainability for companies. Although there is a legal constraint, companies should view it as an opportunity to structure their sustainability strategy and governance.

A 2022 McKinsey survey revealed that 94% Chief Officers admitted that their ESG responsibilities increased compared to three years prior and 47% of them indicating that the increase in responsibilities was significant. The time spent on sustainability matters has also increased, indicating that a pattern is clearly identifiable. ESG importance is spreading across the companies, impacting more and more functions and industries.

We identified that by structuring your sustainability strategy and governance according to new legal framework, internal benefit can first arise by helping to increase efficiency and boost performance through identification of cost savings opportunities. Moreover, the probability of attracting talents and keeping them motivated, especially millennials, is very high. Additionally, complying with CSRD enhances the chances of attracting capital by reassuring investors with a long-term vision.

Some external benefits are also most likely to occur while structuring your sustainability strategy and governance. The brand reputation is expected to improve, representing a major competitive advantage by enabling organisations to build stronger stakeholders relationships. Furthermore, an increased focus on agility is likely to result, improving capacity to anticipate and readily adapt to new regulations. Finally, by developing more innovative and sustainable products and services, organizations might end up creating new opportunities and increase sales.

All arguments are thus gathered to take the best out of the mandatory regulations and create opportunities. But where to start?

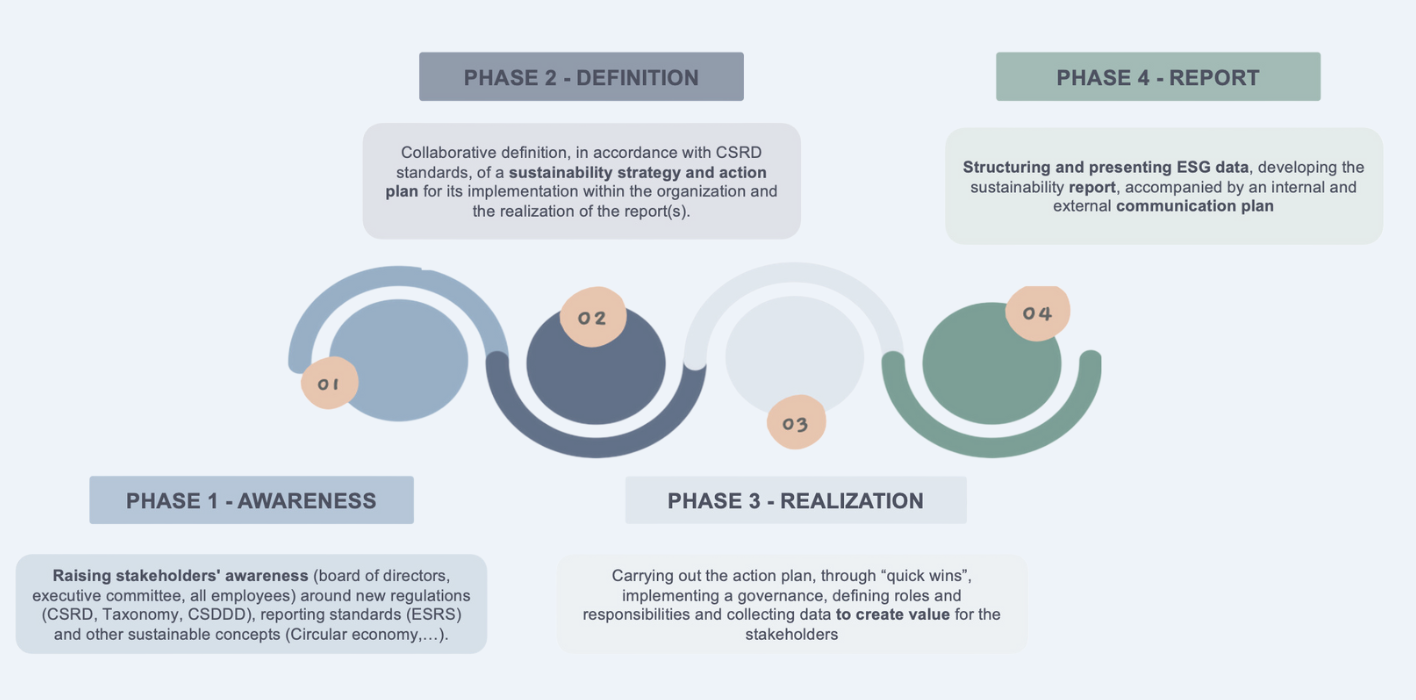

In our sense, your sustainability reporting journey should consist in four phases: (1) the awareness phase, (2) the definition, (3) the realization and (4) the report of information.

1. Awareness phase

As sustainability reporting is a relatively emerging topic, and that it requires deep knowledge of the various sustainability subjects and impacts, the awareness phase should not be underestimated. This phase involves educating stakeholders about sustainability reporting, how it is relevant and how it can help achieve sustainability goals. Different profiles in the company are concerned:

Firstly, it is important to include the board of directors. As the sustainability strategy will be challenged in the reporting journey, and should be completely embedded with the corporate strategy, it is important to take the time to lay the groundwork, to align expectations and implications from the first report and to gain consciousness about the impact of the company. Secondly, as with the Board of Directors, it is important to lay the groundwork with the Executive Committee to understand the "why", "what" and "how" of the first report. Then, management teams are most likely to be impacted operationally by the new regulations and it is therefore important to integrate them from the start of the project to identify together the areas of work.

The board and executive committee have a critical role to play in setting the strategic direction of the organization and ensuring that your sustainability considerations are integrated into the overall business strategy. The management teams hold a crucial role in CSRD reporting, as they are responsible for data collection and management throughout the process. In addition to overseeing day-to-day operations, they are instrumental in implementing best practices, identifying risks and opportunities, and providing valuable input into the development of sustainability strategies. By taking charge of data collection and management, management teams contribute significantly to the success of CSRD reporting.

Additionally, a parallel awareness journey is highly recommended to be started with all employees as involving them from the start of your sustainability journey is critical to its success. Engaging employees in the awareness phase can help to build buy-in, identify potential champions for sustainability, and ensure that the reporting reflects the values and culture of the organization.

Overall, the objective of the awareness phase is to establish a strong foundation of knowledge and understanding that will support the rest of the sustainability reporting journey.

2. Definition phase

The second phase of sustainability reporting is the "Definition Phase," which is a critical step towards achieving sustainability goals and building a sustainable future. This phase involves several key elements, which include building on the work done in the awareness phase, analyzing the current situation to identify amongst others the missing elements in relation to the relevant Corporate Sustainability Reporting Directive (CSRD) standards.

First, a materiality assessment can be performed, aiming to identify material matters for the company, and if not already done, a carbon footprint assessment can be started too. This process involves data collection and interviews with stakeholders to gain a comprehensive understanding of the company's sustainability situation and its position within its industry and market. The company can use the insights gained from these assessments to identify areas of strength, weakness, and opportunities for improvement. This phase is crucial in defining the company's sustainability goals and developing a sustainability strategy that aligns with its values and priorities.

Then, conducting an impact analysis can be done to identify the most significant sustainability impacts of the organization. The impact analysis should be comprehensive and consider both positive and negative impacts. Moreover, it should involve consultation with key stakeholders, including customers, employees, suppliers, etc. By doing so, a sustainability ambition can be defined based on the results of the impact analysis. The sustainability ambition should prioritize the most significant sustainability issues for the organization and align with its overall strategy and stakeholder expectations. It should also be inspiring, challenging, and measurable to drive continuous improvement.

Finally, this all enables the development of a sustainability action plan that outlines the specific actions the organization will take to realize its sustainability ambition. This plan should be based on the results of the impact analysis and the defined sustainability ambition. Moreover, the sustainability action plan should include clear goals, targets, and timelines, as well as a governance structure for monitoring and reporting progress.

Overall, the definition phase is critical to the success of the sustainability reporting process, as it provides a clear roadmap for developing the report and ensures that the report meets the relevant CSRD standards. The definition phase is critical for setting the foundation for effective reporting. It involves gaining a comprehensive understanding of the organization's sustainability situation, engaging with stakeholders, and prioritizing issues based on their materiality and relevance. This information is then used to design and plan a comprehensive sustainability strategy and roadmap for developing the report and ensuring that it meets the relevant CSRD standards. The sustainability report should be based on this action plan and provide a transparent account of the organization's sustainability performance and progress towards its goals.

3. Realization phase

In the realization phase, the focus is on implementing the approach of the sustainability roadmap by collecting and analysing the data identified in the previous phase, enabling the identification of quick wins, managing the sustainability program's governance, and delivering projects. These quick wins can help build momentum and demonstrate progress toward achieving the longer-term goals outlined in the sustainability roadmap. Step by step, all the actions identified as priority are tackled.

Effective governance management is critical during the realization phase. This involves establishing clear roles and responsibilities for sustainability program stakeholders, setting up regular reporting mechanisms to track progress, and ensuring that the program is aligned with the organization's broader goals and strategies.

Finally, delivering projects is a key part of the realization phase. This involves implementing specific initiatives or actions that are identified in the sustainability roadmap. Projects may involve implementing new processes, upgrading equipment, investing in new technologies, or engaging stakeholders in new ways. Successful project delivery requires strong project management skills, effective communication and collaboration, and the ability to navigate any challenges or obstacles that may arise.

By successfully executing the realization phase, organizations set up a solid basis for the reporting and make tangible progress towards their long-term sustainability goals while also enhancing their reputation and creating value for stakeholders.

4. Reporting information

This fourth step is the final step and culmination of an important preparatory process.

The reporting information phase involves structuring and presenting ESG data to stakeholders, including environmental data such as greenhouse gas emissions, energy consumption, water use, waste generation, etc. but also including social responsibility such as diversity, anti-corruption and bribery, etc.

To ensure the credibility and accuracy of sustainability reporting, the Corporate Sustainability Reporting Directive (CSRD) must be followed, providing guidelines and standards for ESG reporting, and ensuring that the information disclosed is relevant, reliable, and comparable across organizations and industries.

Once the ESG data is collected and analysed, it needs to be presented in a clear and concise manner to stakeholders through your sustainability reports, annual reports, websites, or other communication channels for instance. The information should be presented in a way that is accessible, relevant, and understandable to stakeholders, including non-experts. Visual aids such as charts, graphs, and infographics can help to convey complex data in an easily digestible format.

Conclusion

In conclusion, the legal framework established by the European Union regarding sustainability reporting represents a valuable opportunity for companies to structure their sustainability strategy and governance. By doing so, they stand to reap internal benefits such as enhanced efficiency, cost savings, and talent attraction and retention, as well as gaining the trust of investors. Furthermore, external advantages such as improved brand reputation, stronger stakeholder relationships, and increased sales of sustainable products and services may also be realized.

To embark on the sustainability reporting journey, it is crucial to take into account the four phases outlined above. Nevertheless, it is equally important to adopt a broader perspective that encompasses embedding sustainability in the company's daily activities and overall strategy. Given that sustainability reporting is an ongoing process, companies should strive to continuously improve their sustainability performance by providing annual reports and reinforcing their sustainability practices over time.